A Decade of CIF: What the Data Really Tells Us About School Estate Priorities

For many schools and trusts, the Condition Improvement Fund (CIF) has been the difference between managing decline and being able to invest meaningfully in the estate.

Over the last decade, more than 14,500 CIF projects have been approved across England, representing billions of pounds of investment into ageing and often overstretched education buildings. At Warneford Consulting, we wanted to step back from the annual announcements and look at the bigger picture. Not just who won funding, but what types of projects the Department for Education has consistently prioritised over time.

What emerges is a clear long-term shift away from traditional building-envelope works and towards projects centred around safety, compliance and critical infrastructure risk.

Methodology and assumptions

Actual contract costs are not publicly available and so assumptions have had to be made. Annual average project value has been estimated by dividing the total published CIF award funding for each year by the number of successful projects in the dataset for that year. Category-level funding values should therefore be viewed as indicative rather than exact spend.

To allow meaningful comparison across the decade, all values have been adjusted into real 2026 prices using CPI modelling. The purpose of the exercise is not to produce perfect accounting accuracy, but to identify long-term directional trends in how CIF funding has evolved over time

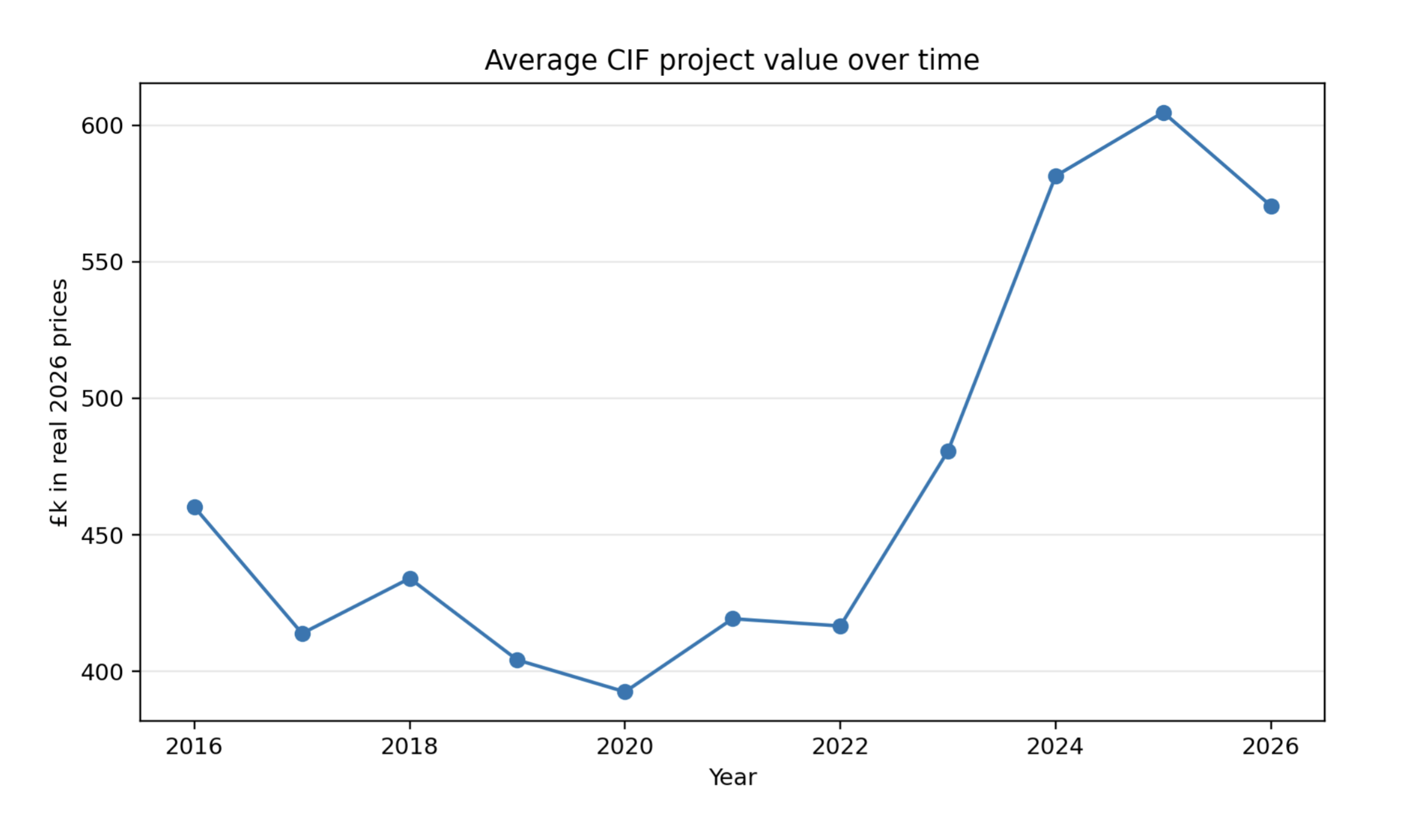

Annual funding and average project values

The sharp increase in average project value from 2023 onwards remains one of the more significant features of the dataset.

Part of this reflects wider inflationary pressure across construction and estates delivery, but it also suggests a continued shift toward larger-scale, more complex and often compliance-led schemes. Schools are increasingly dealing with projects tied to critical infrastructure risk, statutory obligations and operational resilience rather than isolated condition defects.

That changing profile matters because it alters not only the scale of funding requests, but also the level of evidence, strategic planning and risk justification required to secure successful outcomes.

Table 1 shows the annual project count, published funding total and implied average project value.

| Year | Projects | Funding (£m nominal) | Funding (£m real 2026) | Avg project (£k real 2026) |

| 2016 | 1334 | 435.0 | 613.8 | 460 |

| 2017 | 1647 | 496.0 | 681.6 | 414 |

| 2018 | 1589 | 514.0 | 689.7 | 434 |

| 2019 | 1439 | 441.2 | 581.6 | 404 |

| 2020 | 2104 | 631.7 | 825.8 | 392 |

| 2021 | 1486 | 489.3 | 623.0 | 419 |

| 2022 | 1449 | 517.0 | 603.7 | 417 |

| 2023 | 1058 | 467.0 | 508.5 | 481 |

| 2024 | 857 | 469.5 | 498.3 | 581 |

| 2025 | 798 | 470.0 | 482.6 | 605 |

| 2026 | 801 | 457.0 | 457.0 | 570 |

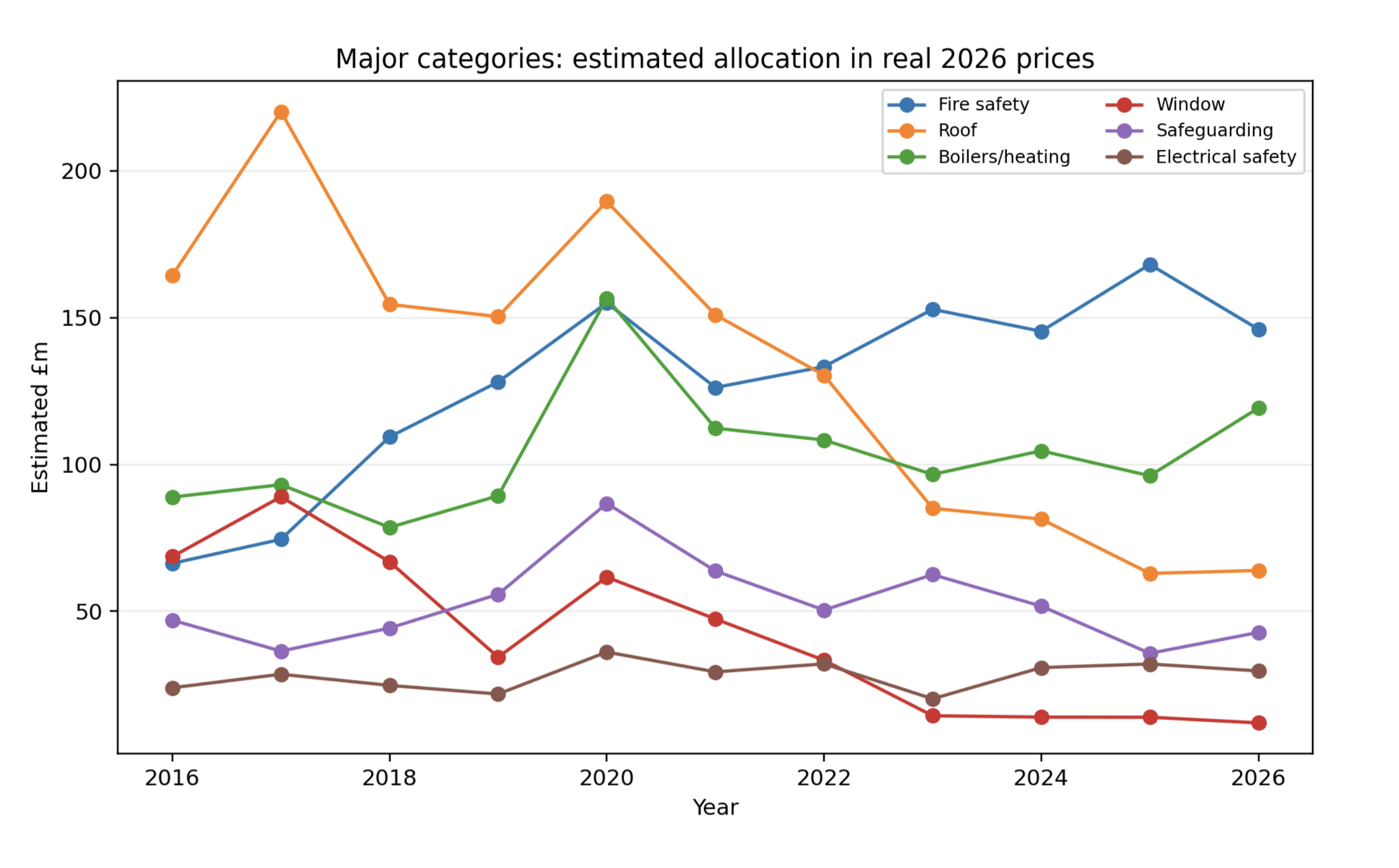

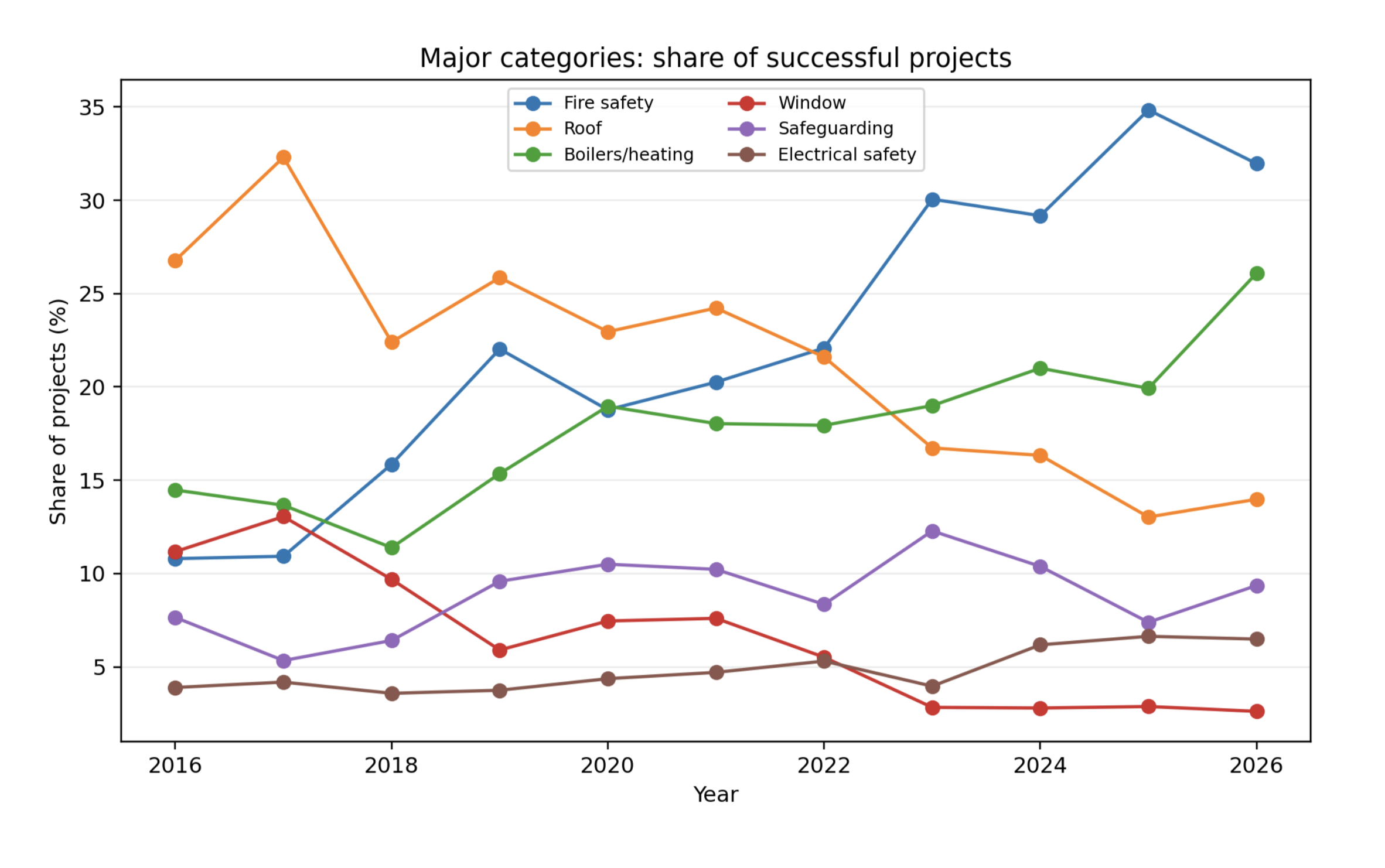

Fire safety

Fire safety remains the strongest growth category in the whole dataset. Its share rose from 10.8% in 2016 to 32.0% in 2026. Estimated real allocation increased by roughly £79.7m across the period.

Roofing

Roof continues its long-run decline. Its share fell from 26.8% to 14.0%, and estimated real allocation fell by roughly £100.5m.

Boilers/heating

Boilers/heating remains one of the core CIF themes and strengthened in 2026. It rose from 14.5% of projects in 2016 to 26.1% in 2026.

Windows

Window work shows a strong decline over the full period, from 11.2% of projects to 2.6% in 2026.

Safeguarding

Safeguarding remains material but more cyclical than directional. It stands at 9.4% of projects in 2026.

Electrical safety

Electrical safety trends upward from a lower base, rising from 3.9% of projects in 2016 to 6.5% in 2026.

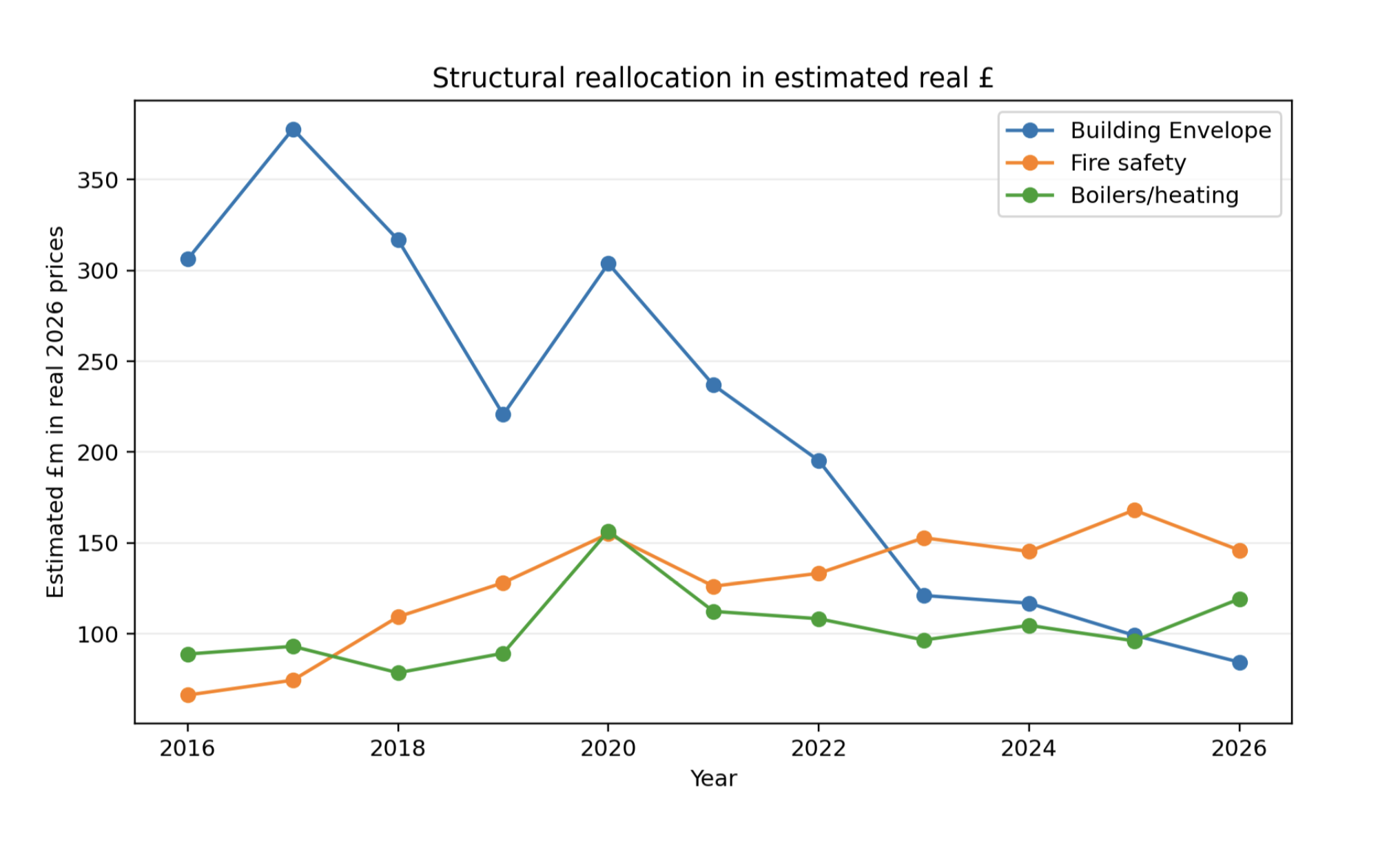

Grouped category view

The broader grouped picture perhaps tells the story most clearly.

When combined into a wider ‘Building Envelope’ category – including roofs, windows, repairs, refurbishment and replacement works – estimated real allocation falls from approximately £306m in 2016 to around £84m in 2026.

That contrasts sharply with fire safety, which rises from around £66m to £146m over the same period.

Taken together, the data suggests a gradual but significant reallocation away from traditional envelope-led remedial work and toward projects centred on safety, compliance and operational infrastructure.

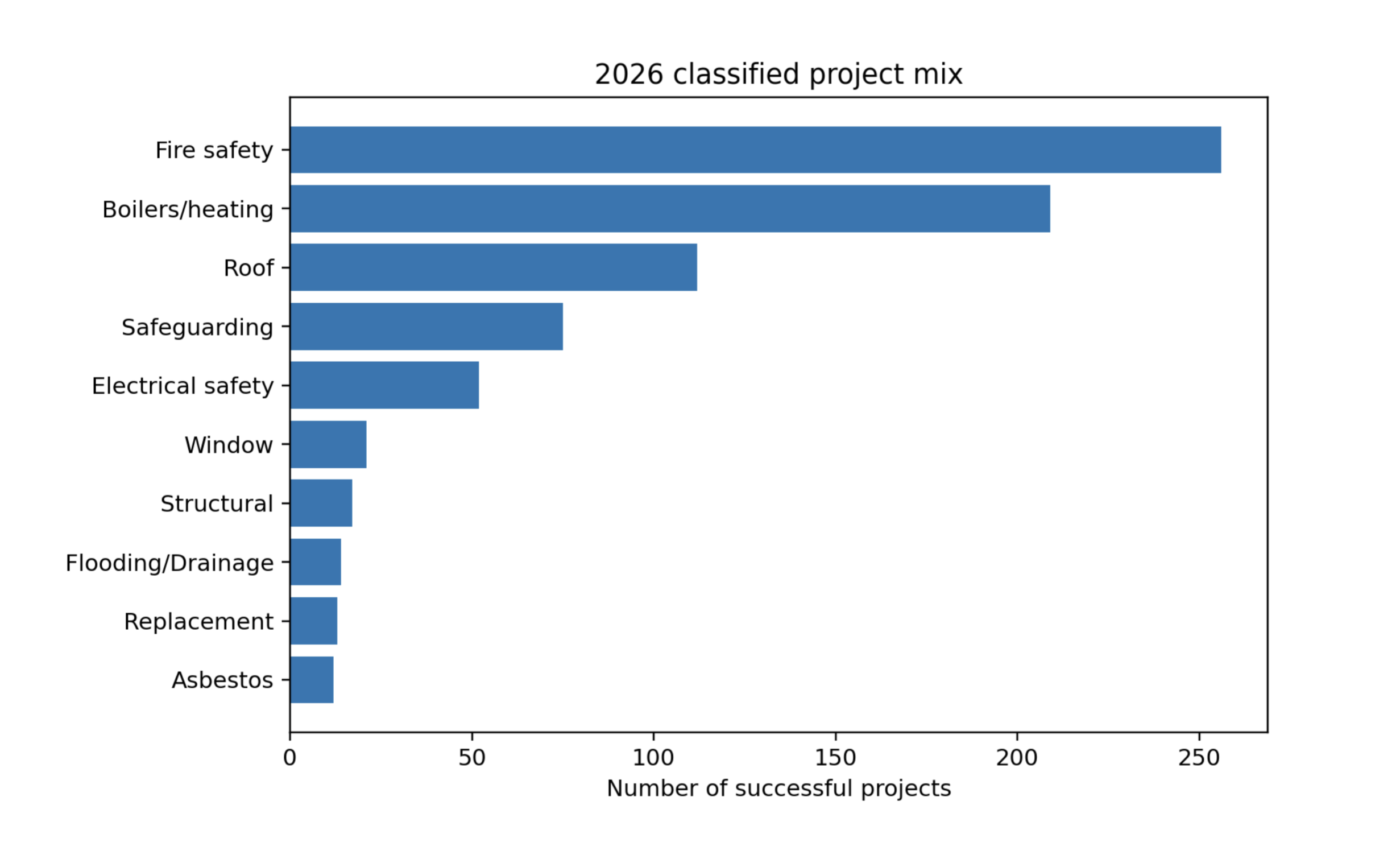

2026-2027 CIF Awards

The 2026-27 allocation continues many of the trends that have been building across the decade.

Fire safety remains dominant. Heating and infrastructure projects continue to perform strongly. Traditional fabric-based works appear comparatively less prominent within the overall mix.

With what is likely to be one final round of CIF before the anticipated introduction of a universal School Condition Allocation model from 2028, these patterns may offer an important indication of where DfE priorities continue to sit.

| Rank | Category | Projects | Share % |

| 1 | Fire safety | 256 | 32.0 |

| 2 | Boilers/heating | 209 | 26.1 |

| 3 | Roof | 112 | 14.0 |

| 4 | Safeguarding | 75 | 9.4 |

| 5 | Electrical safety | 52 | 6.5 |

| 6 | Window | 21 | 2.6 |

| 7 | Structural | 17 | 2.1 |

| 8 | Flooding/Drainage | 14 | 1.7 |

| 9 | Replacement | 13 | 1.6 |

| 10 | Asbestos | 12 | 1.5 |

Regression summary

Table 3 summarises simple linear trend tests using estimated real category allocation (£m) against year. The trend testing within the dataset reinforces what is visible across the wider analysis.

The strongest directional signals remain:

- a sustained positive trend in fire safety;

- a sustained negative trend in roofing;

- a significant decline in window-related projects; and

- continued strength in boilers and heating.

These tests are descriptive rather than predictive, but they help distinguish genuine long-term movement from short-term fluctuation or annual funding variation.

High level trends interpretation

What the data ultimately shows is an education estate under growing operational and compliance pressure.

The sustained rise in fire-safety work remains closely aligned to the post-Grenfell regulatory environment and the increasing scrutiny around building risk and safety management. After RAAC, fire safety now appears to sit among the highest-profile risks facing schools and trusts.

At the same time, the decline in roof- and window-heavy categories suggests that traditional fabric renewal is increasingly competing against more immediate compliance and infrastructure priorities. That creates a difficult balancing act for trusts trying to maintain ageing estates while also responding to changing policy expectations.

There is also a wider strategic question emerging around sustainability and net zero. While envelope improvement and thermal efficiency remain essential to long-term decarbonisation, current funding patterns suggest many schools are still focused on addressing urgent operational risks first.

At Warneford Consulting, we work closely with schools, academies and FE colleges to help shape evidence-led estate strategies, prioritise risk and develop capital funding bids that align both with organisational need and the evolving direction of DfE investment.

If you are preparing for future CIF rounds, reviewing estate priorities or thinking more strategically about long-term capital planning, we would be happy to have a conversation.